The Great Debate – Are SAFEs Actually Bad for Investors?

I’ve heard many people — ranging from investors to attorneys to funding portals — make the claim that “SAFEs are not safe for investors.” Many of these critics will tell you that SAFEs (Simple Agreements for Future Equity) should be avoided as they may never convert to shares. While there is a seed of truth to this conversion concern, we’ll show today that this shouldn’t be a major driver of your startup portfolio returns.

I invest quite often in SAFEs myself. In fact, SAFEs are my most prominent security type in my portfolio of 200+ startup investments; my KingsCrowd portfolio analytics currently state that I have more than 50% of my 172 Reg CF investments in SAFEs (a total of 90, and most of my Reg D investments are also via SAFEs). Thus, I personally believe that SAFEs can be a perfectly fair financial security when used appropriately.

As with many contentious topics these days, the actual truth about SAFEs is much more nuanced and cannot be boiled down to a dogmatic statement such as all SAFEs are bad.

In this article, we will explore the pros and cons of investing via a SAFE vs. equity, why we believe that investors may hurt their potential returns if they avoid SAFEs, and how wise crowdfunding investors should look at SAFEs when investing in startups.

For a brief history of SAFEs, basic deal terms, conversion examples, and differences between traditional Y-Combinator SAFEs and crowdfunding SAFEs, check out our article on crowdfunding SAFEs vs. traditional SAFEs.

Pros and Cons of Investing Via a SAFE

The pros and cons of a SAFE first depends on your perspective. For example, SAFEs are typically considered very founder-friendly, which is much of the reason why they were created by Y-Combinator in the first place. The advantages of a SAFE for founders and entrepreneurs are discussed here.

From an investor’s perspective, some of the pros of investing via a SAFE are:

- Simplicity and ease of execution – this can vary depending on the SAFE, but typically you won’t have any complicated deal terms or provisions that you might see with equity, especially preferred stock, such as liquidation preferences, ratchet provisions, etc. This means funding rounds are easier to execute and can be faster to close.

- Provide founders with more flexibility – for smaller, earlier funding rounds, taking on excessive debt can lead to cash flow issues for startups that haven’t yet made it to product market fit or found profitability. So how is this a pro for investors? Because SAFEs don’t have an interest rate or maturity date like debt or convertible notes, they provide more flexibility and runway for the founders to find that early product market fit without incurring the costs and time of doing a formal priced round.

- Liquidation waterfall priority – in many (but not all) instances, SAFEs are treated on par with preferred stock in the event of a liquidation. This means that SAFE holders may be paid out prior to Common Stock holders, but still junior to creditors and debt-holders.

- Potentially less dilution – I haven’t heard this discussed anywhere else before, but I’ve seen first-hand how some of my crowdfunding SAFEs that choose not to convert at the very next funding round can result in me holding more equity in the end when it does convert. This is an option with some SAFEs (such as Republic), where the founders can choose whether or not to convert SAFEs under certain circumstances. By deferring SAFE conversion to a later funding round, that means that SAFE holders won’t be diluted by any subsequent funding rounds until it does convert to equity.

While some of the above benefits may be attractive to investors, it is also important to consider the potential cons of investing via a SAFE instead of stock:

- You won’t receive any dividends – this shouldn’t be a major consideration for most startup investors, especially since most startups are better off reinvesting capital rather than paying out dividends. However, SAFE holders won’t be eligible if there are any dividend distributions.

- Potential loss of QSBS tax advantages – investing in startups can offer some massive tax saving opportunities for investors under IRC Section 1202 (gains), 1244 (losses), and 1045 (rollovers). One reason that a SAFE is inferior to equity in this case is because one of the stipulations to take advantage of these tax savings is that the startup investment must be in actual equity ownership. Since a SAFE is an agreement for future equity, many tax attorneys believe that the 5-year qualified small business stock (QSBS) clock doesn’t start until a SAFE is converted to equity. However, this is another area of contention, as the latest Y-Combinator post-money SAFE specifically has a clause that states it is to be treated as equity for the purposes of Section 1202. This is not tax advice – always consult your professional tax advisor.

- Lack of voting power – only equity holders (Common and Preferred) will have voting rights. SAFE holders do not come with these voting rights. However, this is less of a con in equity crowdfunding deals, since smaller crowdfunding investors won’t generally get voting shares anyway, even if it was offered via equity.

- Potentially less liquid – while startup investments are inherently illiquid, sometimes SAFE conversion paperwork can unrestrict your shares under Rule 144 (if your SAFE is considered a restricted security – which may or may not apply to equity crowdfunding). That being said, there aren’t many options to sell startup securities via secondary markets today anyway, so this shouldn’t be a major consideration for startup investors who are investing for the long-run.

Note that “lack of conversion to equity” didn’t even make my list of cons. In fact, it appears on the list of pros, since a deferred conversion to equity can ultimately lead to less dilution in some situations.

But What if my SAFE Never Converts to Equity?

Because a SAFE lacks a hard maturity date at which a convertible note would typically convert to equity, many investors automatically jump to the conclusion that “SAFEs run the risk of never converting”.

Yes – that is true.

But for the typical SAFE (reminder: always read your specific deal terms!), your investments that never convert will end up being your failures and zombies, which would have returned less than 1X your invested capital anyway. Meanwhile, your SAFEs that do convert (due to a major fundraising round, acquisition, or IPO) will be your winners.

So how are those outcomes substantially different than if you held stock in those failures and successes instead of a SAFE? The answer: they’re not substantially different outcomes. That’s how SAFEs were designed to act.

Companies that fail will see their stock values go to near-zero (or be locked up indefinitely with no exit plan) – which ultimately is a similar outcome to a SAFE that doesn’t convert. You can write off the investment as a loss (albeit with potentially fewer tax advantages than if you held equity in a qualifying small business under Section 1244).

What if the company is acquired or sold before your SAFE converts? Most SAFEs will still be treated as non-participating preferred stock, so you’re covered there, too.

All this being said, there are very rare examples of SAFEs and Convertible Notes that high-profile investors held which never converted, so it is possible. See the TopTal example here, where investors such as Andreessen Horowitz and others weren’t converted when they arguably should have been.

So the risk isn’t non-zero.

But in my personal opinion, investors put their portfolios at greater risk of subpar portfolio returns by avoiding SAFEs because they will potentially miss out on several deals that provide massive returns (see below discussion about errors of omission).

If SAFEs are trusted by some of the top angel investors, VC firms, and accelerators, then it’s safe (no pun intended) to say that some of the best startups in the world will choose to use them. And I don’t want to miss out on those opportunities.

The biggest takeaway for investors is this: all SAFEs are NOT created equal. Always read specific deal terms for any deal – whether that deal is SAFE or Common/Preferred Stock – as the devil is always in the details of the deal terms.

Some example deal terms to watch out for in any security are repurchase rights or redemptive clauses. While some earlier SAFEs were notorious for these investor-unfriendly deal terms, I have also seen repurchase rights on Common Stock. That’s why it’s crucial to always read the fine print.

Why Avoiding SAFEs Can Hurt Your Investment Returns

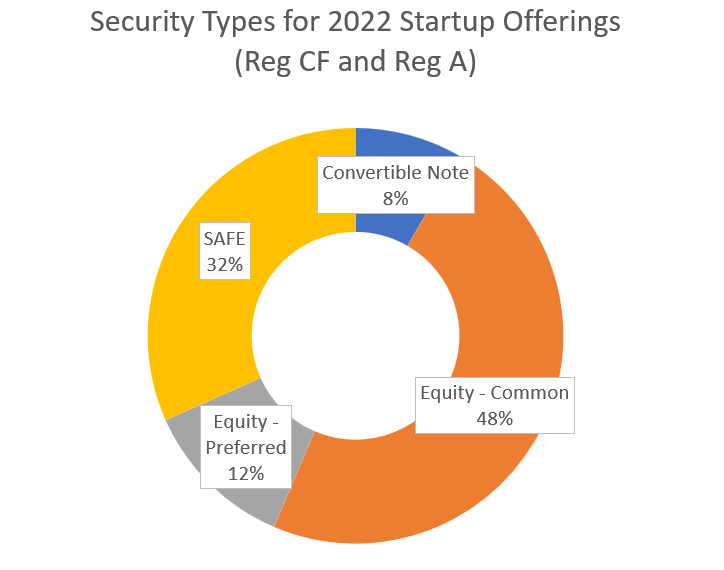

First, a quick statistic: in 2022 online startup investing (Reg CF and Reg A+), 414 out of 1308 equity deals were SAFEs, meaning that SAFEs accounted for 32% of online startup investing deal flow (and 37% of total capital raised in 2022 was done via SAFEs).

If you’ve been following startup investing and have read all the angel investing and VC books out there, you understand that it’s nearly impossible to determine which startups will succeed and which will fail in the early stages (and arguably in the growth and late stages as well). Thus, it’s reasonable to assume that at least a few of the future 100X+ startup returns likely reside within that 31% of startup deal flow offered via SAFEs.

Therefore, it’s also reasonable to conclude that if you simply avoid all investment opportunities that are SAFEs, you are likely submitting yourself to omission bias (aka errors by omission). Omission bias is where we tend to judge harmful actions (e.g. losing 100%) as being worse than harmful inactions (e.g. missing out on 1000% gains).

In the context of startup investing, this means you will potentially miss out on some of the most lucrative startup investing returns. As we have discussed, power law returns are the primary driver of startup investing portfolios. So what if the Uber, Facebook, or Airbnb of tomorrow happened to be one of those SAFE offerings?

Think of it this way: what’s worse for your portfolio – losing 100% on several complete failures, or missing out on a single 100-1,000x gain that you didn’t invest in (hint: it’s the latter, which more than makes up for all your failures). For example, check out this analysis we did a few years ago on Wefunder’s Reg D deals and see how the returns differ at the time if you had missed out on Zenefits.

It’s Peter Theil’s famous quote in action:

The biggest secret in venture capital is that the best investment in a successful fund equals or outperforms the entire rest of the fund combined. – Peter Thiel

SAFEs are Not the Issue – Bad Deal Terms are the Issue

SAFEs are a tool for raising capital. As with any tool, there is a right and a wrong way to use this financial security.

SAFEs also come in many different flavors. So it’s unfair to issue a blanket statement such as “all SAFEs are bad for investors”.

I have seen “unsafe” terms for investors — such as repurchase rights (covered in more detail in the video here) — in other supposedly “safe” securities, such as Common Stock and Convertible Notes.

Thus, simply recommending that investors avoid SAFEs to avoid bad deal terms can lead those same investors to a false sense of security. SAFEs are not the real problem. Bad deal terms are the problem.

SAFEs are Used Industry-Wide by Top Investors and Platforms

It’s no coincidence that two of the top three funding portals, Wefunder and Republic, both strongly encourage their issuers to use SAFEs. Or that the most well-known accelerator in the world (and the inventor of the SAFE), Y-Combinator, uses SAFEs. Or that AngelList syndicates, Jason Calacanis’ syndicate, and countless other angel investors use SAFEs.

If you look at some of the most successful Wefunder Reg D companies from 2013-2016, 4 of the top 5 were on SAFEs, and 2 of those were even on uncapped SAFEs; so investors who avoided that would have missed out on 4 companies that all generated 12X-34X gains and would make a difference in a startup portfolio.

As with anything in startup investing, I look at SAFE investments as another form of diversification. In the end, it’s up to each investor’s individual risk tolerance, investment goals, and the specific deal terms as to whether or not investing in a SAFE might make sense.

Additional Resources

FINRA has a page dedicated to SAFEs here.

Responses