The Republic Note Token – Is It a Good Investment?

2023 Update:

- As of April 10, 2023, Republic has re-launched the Republic Note as a “digital security” and at a new offering price of $0.36/Note, a 3X increase in price from three years ago when this article was originally written. There is currently a $2M allocation available under Reg CF to non-accredited investors on these terms, while there is a separate allocation under these terms available to accredited investors under the Reg D offering.

- While the original Reg A (testing the waters) offering from July 2020 still hasn’t been qualified by the SEC (and seemingly taking much longer than Republic had hoped), Republic honored some of those earliest reservations by having a very limited allocation of $3M under Reg CF in February 2023 available to those investors who had reserved Notes in the original Reg A offering at the original 2020 price of $0.12/Note.

- The new April 2023 Note offering provides new details about portfolio company updates (both on the retail platform and through Republic Capital), as well as exciting details about community benefits for Note holders and anticipated deadline for the Republic Wallet (estimated Q2-Q3 2023) and Note distribution.

- Republic disclosed some extremely interesting and useful information as part of their Form C filings for these Reg CF Note offerings – check out the 2023 offering paperwork here (189 pages long). Pages 48-64 may be of particular use to investors who want to see Republic’s portfolio company holdings and adjust assumptions used in the original article below.

Original article from July 2020:

On July 16, 2020, Republic officially launched its sale of the Republic Note profit-sharing token at a price of $0.12 per Note token. Accredited investors can purchase the tokens under Reg D as of July 16, while non-accredited investors have to reserve their allocation of tokens and wait until the approval of the Reg A offering later this year.

While there is no arguing that Republic’s Note token is innovative and pushing the industry forward, everyone has been asking me one question over the past few weeks. Is the Republic Note token a good investment?

While this article is not investment advice and investors have different goals and risk tolerances, we will attempt to provide an independent analysis of whether the $0.12 per Note price is fairly valued or not for investors. We will perform a Discounted Cash Flow (DCF) analysis for optimistic, typical, and pessimistic scenarios to arrive at a rough valuation range for the Republic Note token.

To download a copy of the financial modeling spreadsheet and be able to tweak all the numbers and assumptions yourself, log in (or create) a free Crowdwise account and then click the link below (only visible to logged-in members).

Also, here is a 30-minute video overview of the Republic Note valuation spreadsheet and assumptions:

What is the Republic Note profit-sharing token?

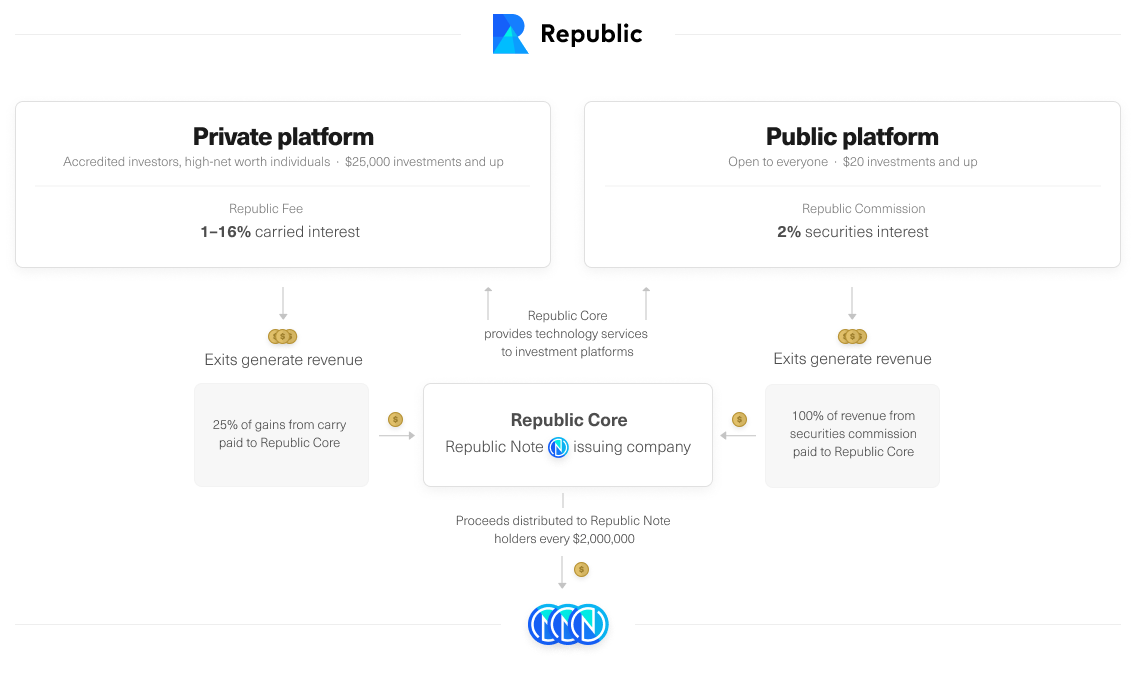

At a high-level, the Republic Note is a profit-sharing token that is intended to share profits from successful portfolio companies on Republic’s public and private crowdfunding platforms. While the value of the Republic Note token will be volatile and traded on secondary exchanges such as Binance in the future, each Note token entitles the holder to dividend payouts (in stablecoin) whenever Republic’s profits from successful companies exceed $2 million.

Below is an overview of the profit-sharing model. It is a very intriguing structure because it will essentially allow non-accredited investors to share in profits from Republic’s Private platform companies, which are usually restricted to only accredited investors.

Since we will solely focus on valuing the Republic Note token and not on all its other details and risks, we strongly recommend that potential investors sign up to be notified on July 16, read the whitepaper and FAQs, and check out some of our AMA questions and answers from Republic’s CEO, Kendrick Nguyen.

Why Does Valuation Matter?

“It’s not what you buy that determines your results, it’s what you pay for it.” – Howard Marks

I’ve heard many investors exclaim their enthusiasm about the Republic Note and their eagerness to invest in it because it is so innovative and promising.

While I do not disagree with their enthusiasm and optimism, one of my favorite quotes from Howard Marks reminds us that it isn’t only the financial security that you buy that determines your investment results; it’s the price that you pay for that financial security, whether that be stocks, bonds, real estate, or other alternatives such as crypto or startups.

The Republic Note is being offered at $0.12 per Note. According to the whitepaper, investors in Q3 2018 and 2019 invested at Note prices ranging from $0.06 to $0.10 per Note.

So, is $0.12 per Note fairly valued? What if it was $12 or $0.01 per Note? Would it be a good investment then? This is why we will perform an independent, bottoms-up valuation of the Note token to see if it is reasonably priced for investors.

How did Republic arrive at $0.12 per Note?

During the AMA with Republic’s CEO Kendrick Nguyen, I was able to ask him how Republic arrived at $0.12 per Note. Kendrick’s response was:

Kendrick: “We took a look at how other major projects value their total network and apply a significant discount. Afaik, Republic Note is the first project with this large of a community with network value under $100M”…”As with all projects, today’s valuation takes into account future growth, and future growth projection takes into account past growth. We subjectively believe that our network value is priced well below market – loosely defined by comparing against other major networks.”

Thus, while there were no concrete valuation methods provided, it sounds like Republic may have used a combination of some lower-level growth assumptions with some higher-level, subjective network value assumptions to arrive at what they believe is a fair price of $0.12 per Note.

Republic Note Valuation – Key Assumptions

In setting up our DCF analysis of the Republic Note, we had to make numerous assumptions about early-stage investment returns. This is because the distributions to Note token holders is 100% dependent on profits from Republic’s public crowdfunding business (based on the 2% equity stake Republic gets) and 25% of profits from Republic’s private platform.

In other words, the primary drivers of the financial model are:

- The number of companies on Republic’s public and private platforms

- The growth rate of the number of companies on Republic’s platforms

- The potential returns of companies on Republic’s platforms

While we can make educated guesses in terms of #1 and #2 above, it’s highly unlikely that even Republic can know with 100% accuracy how many companies per year they will have on their platform in a few years from now. Republic’s portfolio currently consists of 29 and 133 companies on their private and public platforms, respectively.

For #3 – the potential returns – we used a range of average portfolio IRRs from angel investing and early-stage VC data and assumed an average five-year exit timeline. These overall portfolio IRRs account for failure rates of early-stage companies, so we did not have to assume a certain failure rate for this analysis.

Specifically, our model assumed the following for returns:

- Optimistic – 25% IRR for public platform cumulative returns; 20% IRR for private platform cumulative returns (assumed slightly lower due to later-stage companies on the private platform)

- Typical – 15% IRR for both public and private platform cumulative returns

- Pessimistic – 5% IRR for public platform cumulative returns; 10% IRR for private platform cumulative returns (assumed a higher relative pessimistic IRR due to an anticipated lower failure rate due to slightly later-stage companies on the private platform)

Secondary assumptions to our financial model that we included were:

- Total number of Republic Notes in circulation (we assumed the maximum amount of 800,000,000 for the below results to be conservative)

- Potential fees and taxes on profit distributions to Note token holders (surprisingly, the final returns weren’t very sensitive to fees, even if Republic took anywhere from 1-10% in fees for each $2M distribution)

- Discount rates are used to obtain the present value of future cash flows (assumed 10% discount rate for the results below – i.e. $1,100 in a year from now is only worth $1,000 today)

Upper, Middle, and Lower Bound Estimates for Republic Portfolio Company Growth

In addition to the range of potential returns mentioned above, we also varied the potential growth rate of the number of companies on Republic’s platforms. We assumed the starting number of companies on Republic were 29 private companies and 124 public companies and that the annual growth rates of number of companies on each would be:

- Optimistic – 35% annual growth rate (e.g. 100 companies in year one would add 35 new companies in year two, 47 in year three, etc.)

- Typical – 20% annual growth rate

- Pessimistic – 5% annual growth rate

In reality, it is likely that Republic could grow the number of companies much quicker in the near-term and then slow down in the long-term (e.g. at 30% growth, it’s much easier to go from 100 to 130 companies rather than from 1,000 to 1,300 companies).

In addition, we imposed a cap on the maximum number of new companies per year that we thought would be sustainable by the Republic team. Again, this will be very dependent on the growth of the Reg CF industry overall, the success of Republic as a funding portal vs. their competition, and the size of the team that Republic decides to hire to sustain that growth (or not).

We chose 200 companies per year as the upper limit for the public platform and 100 companies per year as the limit for the private platform. Thus, it is likely that Republic could see an even larger potential upside in the future if they build a team and system capable of on-boarding more than 200 companies per year.

Republic Note Valuation – The Results

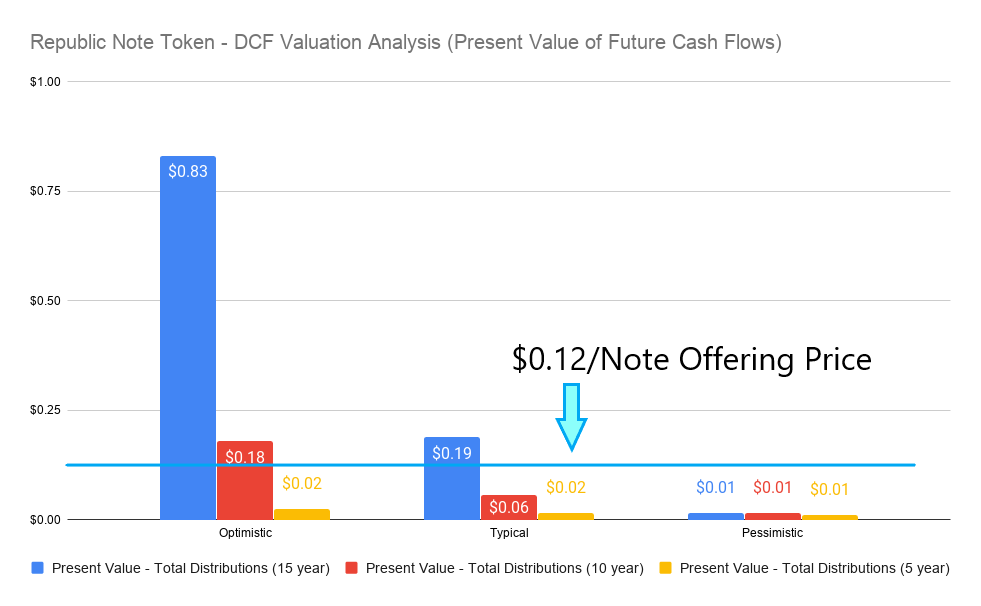

After tweaking our assumptions and constructing the DCF analysis, here are the upper, middle, and lower-bound estimates of the present value of the Republic Note token’s future cash flows based on our analysis. We put the results in buckets of 5-year returns, 10-year returns, and 15-year returns since the potential payouts will be depending on the growth of the number of companies on Republic’s platforms.

Here are a few takeaways from the above results:

- The above chart is the present value of future cash flows only, and does not account for any appreciation or depreciation in price of the Note token itself. That is, if the price of the Note token traded on secondary markets goes from $0.12 to $0.24 due to demand, the chart does not account for the fact that you doubled your original investment amount.

- The potential value of the Republic Note is very dependent on growing a large number of Republic portfolio companies in the future. Even in the most optimistic case, the estimated distributions in the first five years of the Note token are expected to be very little – about 1-2 cents per Note. This is because it takes early-stage companies 5-9 years on average to exit, and Republic’s portfolio companies are only a few years old. It will take time and momentum to build a portfolio that provides consistent exits for Note holders.

- Even when looking at a 10-year investment horizon, only the optimistic case has a higher present value of future cash flows than the offering price of $0.12 per Note.

- The above chart assumes that all 800,000,000 Notes were in circulation from Day 1. Having half as many Notes in circulation at the start means that the early distributions could be higher by a factor of 2.

- The corresponding IRRs for each of the 15-year analyses is 6.1%, 1.7%, and 0.3% for the optimistic, typical, and pessimistic cases, respectively. The bulk of most of those returns happen in the latest years, though, because it depends on the number of companies and how long they take to exit. Again, this only accounts for profit distributions and excludes any assumptions about the future value of the Note token on secondary exchanges.

Based on these assumptions, one could estimate that each Republic Note could take between 10-15 years to break even (i.e. to pay out $0.12+ in dividends), and maybe a little sooner than 10 years under the optimistic case.

However, if you held a bond that paid 3% interest, that would take 23.4 years before breaking even (ignoring redemption value), and yet many investors invest in such instruments. So, based on the above numbers, does that mean the Republic Note is reasonably valued at $0.12 per Note?

Republic Note Updates

Update as of April 2023:

Republic re-launched the Republic Note as a “digital security” and at a new offering price of $0.36/Note, including more details about community benefits and anticipated distribution timelines. This offering is open to both accredited and non-accredited investors. There is $2M allocated under the current Reg CF (which is because of the $5M, 12-month limit on Reg CF and due to the prior $3M raised in Feb. 2023), as well as additional allocation available under a separate Reg D offering.

Update as of February 2023:

Republic launched a very limited allocation of $3M under a Reg CF offering (and a separate Reg D offering), only to investors who had originally reserved Notes back in the original July 2020 offering. The idea was to give these early investors the opportunity to invest at the original 2020 reservation price of $0.12/Note, despite the fact that Republic felt that the Note price was now likely substantially higher (as we saw in the new offering in April 2023 of $0.36/Note).

The original Reg A campaign from July 2020 that was testing the waters has still not been qualified by the SEC, despite Republic’s optimistic attitude each quarter for the past few years. This is likely why Republic decided to go with Reg CF offerings for the Note instead. The SEC’s recent actions against various security tokens and exchanges and crypto in general may also be what led Republic to re-launch the Note as a “digital security”, perhaps to separate it a little more from being seen as a “crypto”-related asset in the eyes of the SEC.

Update as of 7/21/2020:

Republic has announced that as of the first five days of the offering, over $10 million Notes have been reserved. As such, they increased the cap to the maximum allowed of $16 million in Notes. This shows that there has been extremely high demand for the Republic Note.

Also, after talking more with various sources, Republic may actually be looking to onboard 200 (or more) companies next year, as they have been experiencing 2x to 8x year over year growth.

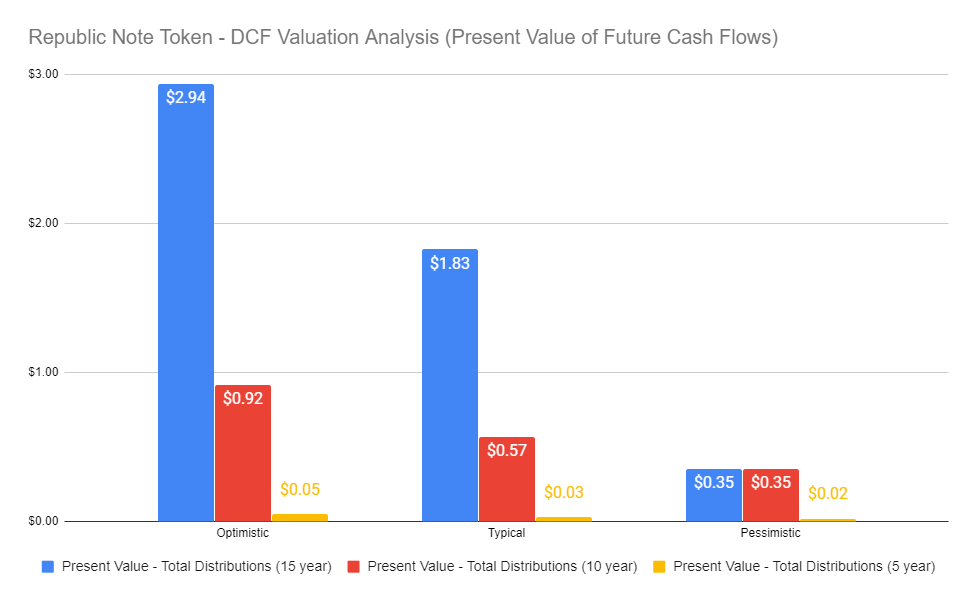

What would the valuation numbers look like if we made the following model updates?

- Decrease the Notes in circulation to be 400 million, which is more accurate for the first few years

- Assume 200 new public companies per year for the next 15 years (conservative assumption that this is constant and doesn’t grow, when in reality it will likely grow)

- Assume 50 new private companies per year for the next 15 years (conservative assumption that this is constant and doesn’t grow, when in reality it will likely grow)

Here are the results of having a higher number of companies on the Republic platform, which paints a more optimistic picture for the 10 year and 15 year potential returns, even for the pessimistic case:

Assuming Republic can bring on 200 companies per year and 50 companies per year for the public and private platforms, respectively, and maintain the level of quality that is typical in angel investing, then the Note could indeed be quite lucrative when those companies begin to exit in roughly five years.

Final Decision – is the Republic Note a Good Investment?

That all depends on your investment goals and projections in terms of how successful Republic will be, as well as how much the Reg CF and Reg D industries grow in the coming years.

It’s worth noting a few things that the above analysis leaves out:

- Supply and demand. The value of the Republic Note token won’t be valued based solely on future cash flows. Supply and demand and investor psychology will come into play, perhaps driving the price up (or down) from the initial $0.12 per Note. Will the price of a Note token rocket to $0.24 or plummet to $0.06 on the first day of liquid trading? Only time will tell.

- Future Republic Core businesses. This analysis assumes that the only profit sources for Republic Core will come from the public and private investment platforms. Republic has hinted that it could add other businesses to the picture in the future, such as their gaming platform, Fig, or their new real estate platform, Compound. Thus, the potential upside could be much higher than what we presented here.

- Risks. If Republic ceases to exist, goes bankrupt, or changes business models – whether that happens next year or ten years from now – that would likely mean that the Note token would eventually become worthless since they won’t be adding new companies. Personally, I’m optimistic about the future of Republic and what they are doing, but anything is possible.

- The value of other community benefits. The Republic Note offers other community benefits and incentives for token holders beyond its monetary and profit-sharing value (such as investor waitlist priority, swag packs, etc.). Thus, the inherent value of the Republic Note may be higher than simply that of its financial potential.

Because of the unique risks of the Republic Note token, you should remember to treat this as any other startup investment and only invest money that you can afford to lose. Even if Republic doesn’t fail, if Reg CF companies fail to perform as well as traditional angel and VC investments, then profits could be much lower than the typical case.

Personally, I have allocated some capital to invest in the Republic Note (about 10X of my standard startup investment check size for now). I think it is innovative and interesting and I would like to see where it leads in the future. My guess is that since the bulk of the value of profit-sharing will come in later years, there may be an initial up-tick in Note price due to interest and supply/demand in the first year or two, but then it may be a few years before people start realizing the potential value of the Note. It will depend supply and demand, so if the initial Notes sell out faster than anticipated (which they are as of 7/21/2020), it could result in the value of the Note going up more in the short-term once it is listed on an exchange.

Is the Republic Note Like a Passive Index Fund for Startup Investing?

Unfortunately, the Republic Note is not yet at the level of being on par with a “passive index fund for startups” – but it is a step in the right direction.

To achieve that, it would have to be something that I could confidently allocate a large chunk of capital towards (say, 5% of my entire investment portfolio), and then I could expect to get returns on par with the early-stage asset class.

The reason that the Note isn’t yet at that level of maturity is because there is still a non-trivial amount of risk that Republic as a company could end up being worthless, shut-down, or reach a dead end due to regulations, in which case the entire portfolio of Notes would become virtually worthless. That is the risk that one takes when investing in startups, but that’s the reason why diversification among many different startups is the key to success. And investing all my startup capital in the Note would be the rough equivalent to betting it all on Republic.

While I’d love something like a passive index fund to allow me to allocate a large chunk of capital and get steady returns and diversification, and while this is a step in the right direction, my personal opinion is that the Republic Note is still part of a nascent company in an evolving industry, so there is a non-zero chance that the entire investment could become worthless.

On the flip side, I do see an asymmetric risk profile by investing in the Republic Note. It has a limited downside (my investment can only go to zero, not below) and an unlimited potential upside subject to the power law; especially if Republic continues to grow and potentially even add other businesses like Fig and Compound to the mix. If you’re optimistic about the future of Republic and the crowdfunding industry in general, it may be worth taking a deeper look at the Republic Note token when it launches on July 16.

Leave your thoughts in the comments section below. What do you think of the Republic Note? As always, I welcome all feedback to help improve and correct my assumptions and financial modeling for the Republic Note, and I may update this page over time as more information becomes available.

Where Can I Learn More and Invest in the Republic Note token?

To learn more and to pre-register your interest prior to the July 16 launch or purchase Note tokens after that date, head over to Republic.co/note.

The initial offering will be capped for both accredited and non-accredited investors, so if you think you might be interested, don’t wait too long to reserve your shares (which will then be available to non-accredited investors later in 2020 after Republic receives SEC approval of their Reg A offering; see the Note whitepaper for more details).

That being said, don’t get caught up in the hype and become a victim of FOMO (fear of missing out) and other psychological investor pitfalls.

Another relevant custom cryptocurrency used to create token through crowdfunding is https://www.mintme.com/

The “IRR” return assumptions should actually be labeled as ROIC assumptions, since you are deriving NPV as the unknown variable based on an assumed ROIC. IRR is the implied % return derived from the timing of net cash flows in order to make NPV = 0. This is just a minor nomenclature issue and doesn’t affect the analysis.

The major issue is the assumed discount rate. A rate of 10% is definitely too low. For mature and established SME companies, which these startups are very far from, a minimum discount rate to adequately reflect the risk involved would be about 15%. Therefore, I personally would not settle for any discount rate less than 25-30% here to reflect the high risk of this investment. I would probably model with a more comfortable rate of about 40%. That would cause a dramatic decrease in all the NPV amounts.